5 Steps to Successful Real Estate Accounting and Bookkeeping for Investing Startups

- September 8, 2020

- admin@ohi

As a real estate manager, you are already aware of the altering aspects of the industry, which makes accounting a tedious task. Especially in this sector, you need to keep track of the myriad of state and national regulations and take care of multiple transactions.

But, we still need bookkeeping and accounting to achieve organized accounts, zero legal complications, and long-term business profitability. When you know your finances and have accurate books, you gain the ability to make better data-driven decisions.

It is amazing that you don’t really need to become the best in accounting and bookkeeping. You only need to understand the basics and start early. Once your business is big and evolving, messy previous records bring in a lot of problems. So, check out the following tips and follow these steps for your real estate accounting to make better financial decisions!

Before we move on, here are some things that you should understand about accounting and bookkeeping.

Below we have discussed some simple yet extremely beneficial real estate accounting and bookkeeping tips for the real estate sector. Using these tips, you can reduce errors in your books, eliminate compliance problems, and improve the efficiency of decision-making.

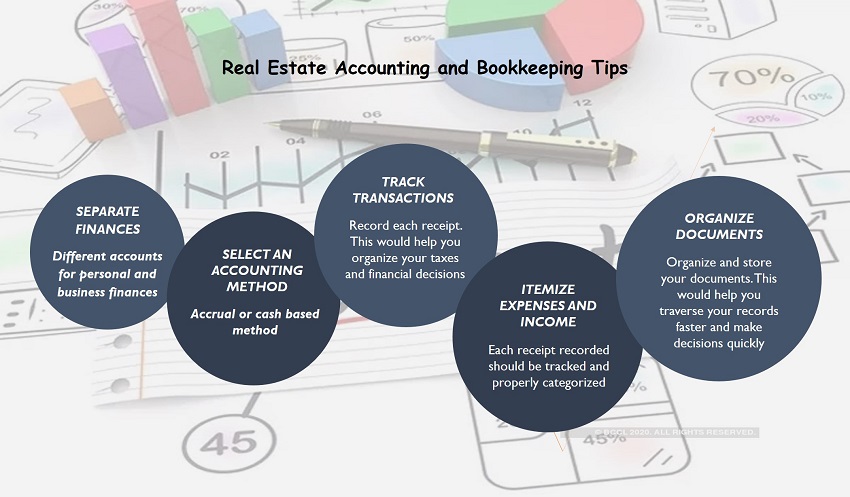

The rule of the thumb is to use different accounts for personal and business finances. Don’t merge these two things to avoid issues in the long-term. If you fail to separate business and personal accounts, you can suffer the following:

With a separate account for personal finances, you can handle your transactions and keep track of finances without any hassle.

Real Estate Accounting and Bookkeeping Tip – When you are a small business, it may seem logical to have a different account for every rental property. However, this is not feasible in the long-term. Think about it, after five years, how would you manage 40 accounts for 40 rental properties?

That’s not practical.

Therefore, it is best to have one account for all your properties. You still need strategies for streamlining rental property accounting separately, but your accounting system would be highly organized in this manner.

Select one accounting method: accrual accounting or cash accounting

Accrual accounting is difficult but essential. You need to write two entries for one transaction. These transactions are opposite and equal.

The cash-based accounting method is simple as when you receive a deposit, you record income, and when you pay, you record expenses.

Both methods have some advantages. Based on your requirements, select the one which is beneficial for your business. Do your research on what other leaders in your industry are using to make this decision.

For every property, record each receipt with the purpose of the receipt. This would help you organize your taxes, deduct accurate taxes, and organize your financial decisions.

It is necessary to note that you can record your transactions in a spreadsheet as well. There’s no need to purchase costly tools or use crucial management techniques. Simply record every transaction and receipt of your properties in a spreadsheet to keep track of data in the long-term.

How should you record transactions?

Every transaction or receipt should be recorded as per government standards. You can take a snapshot and add it to your books. A hard copy is not necessary.

These snapshots would help you during an audit or glitch in tax filing.

Every receipt that you track and record for your business should be tracked and properly categorized. This would help you ensure that bills are clear and you are using the right credit or debit card for every property.

It is best to start itemizing your expenses and income early. The more you delay, the more time-consuming this task will become, and the more errors would be encountered in the system.

Organize the documents that you need to store for your business. This would help you traverse your records faster and make decisions quickly.

Here are the categories:

Make proper folders for these documents to locate these documents easily whenever needed, such as during an audit.

Real estate accounting and bookkeeping can be harder than anticipated. Recording transactions and receipts accurately requires consistent effort. Even with meticulous functioning, you can miss on some factors. Hence, if you are unable to implement the above tips, consider outsourcing your real estate accounting and bookkeeping for precise results and expected outcomes.

OHI is a fifteen-year-old real estate services company working with 50+ commercial and residential real estate developers, funds and property management companies across USA. Our deep expertise in real estate accounting, financial analysis, lease administration and asset management has helped clients cut associated costs by 40-50%. We now provide these services to a portfolio of 75000 units across clients.

We invite you to experience finance and accounting outsourcing through us.

Low Cost Property Accounting Services for Real Estate Investors: AP | AR | Reconciliations | Month End Closing | Financials | Year End Accounting | Reporting – VIEW MORE