Summary Note on 1031 Exchanges

- December 21, 2016

- admin@ohi

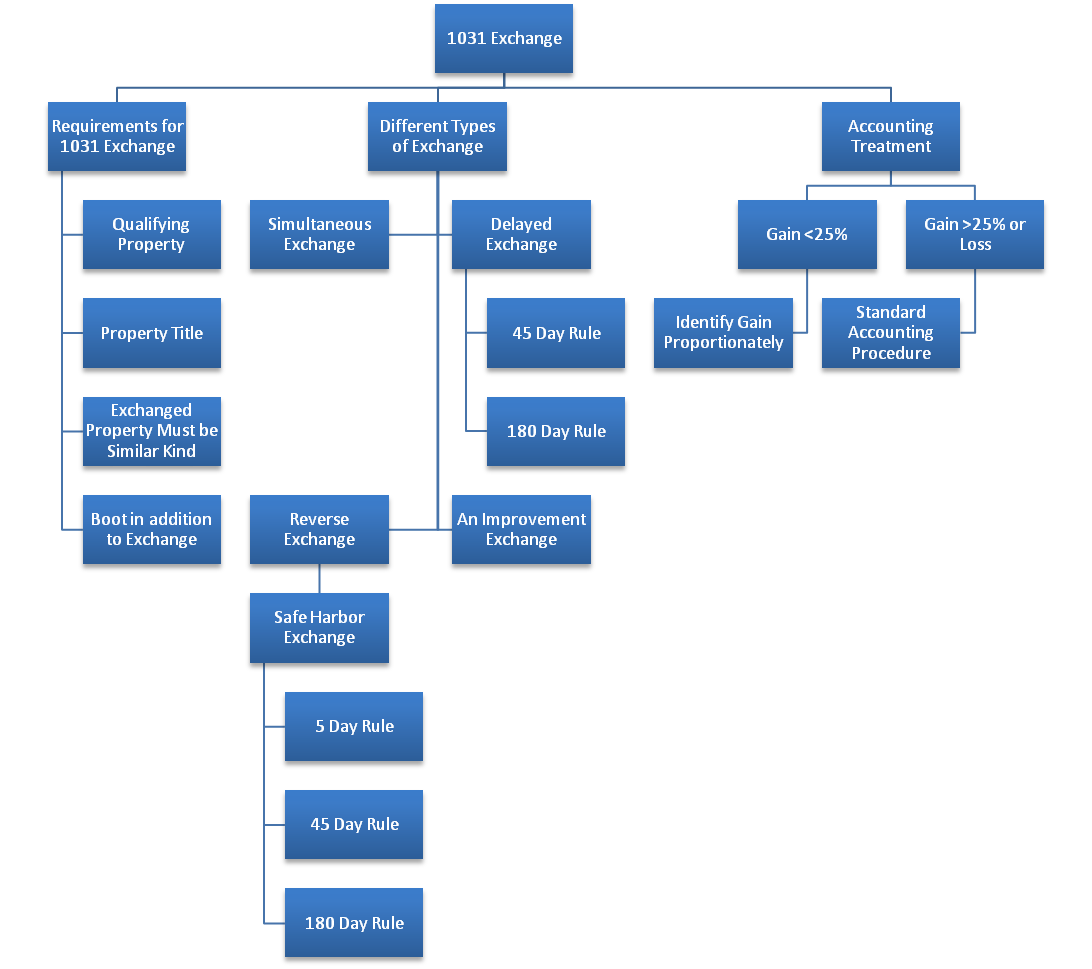

Section 1031 of the IRS Code, commonly known as “1031 Exchanges,” forms the basis for tax-deferred exchanges. It allows taxpayers to defer paying income taxes on the sale of property if the proceeds are reinvested in a similar kind of property. This exchange requires specific conditions to be met, as selling a property and purchasing a replacement property after a gap does not qualify.

While 1031 exchanges offer tax benefits, they come with certain disadvantages, including a reduced depreciation basis for the replacement property. The formula for calculating the depreciation value is:

Depreciation Basis = Purchase Price of New Property – Unclaimed Gain from 1031 Exchange

Additionally, any unclaimed gain from the exchange is taxable in the future if the taxpayer cashes out.

The replacement property must be of a similar type to the relinquished property. Key rules include:

Boot refers to money or debt relief received in addition to the exchanged property. This is taxable to the extent of the gain realized. Common types of boot include:

Example:

A Qualified Intermediary (QI) facilitates the 1031 exchange process by:

While IRS guidelines do not license QIs, certain parties (e.g., accountants, attorneys, or realtors) who have provided services to the seller in the past two years cannot act as intermediaries. Sellers should choose trustworthy QIs to minimize financial risks.

Safe Harbor guidelines offer a framework for compliant exchanges:

Conclusion

Investors usually enter into 1031 Exchange to avoid tax payments on Capital Gain from sale of properties. Parties interested in 1031 Exchange must fulfill key requirements before entering into exchange. Parties can choose from multiple types of exchange as per there situation and needs. The real estate accounting and tax implications vary based on the type of exchanges. 1031 exchanges can be fairly complicated, so its best to engage an accounting and taxation expert to structure the exchange.