40-60% Cost Savings

Skilled Employees

300+ Clients in USA

OHI’s helps start-ups and small mid-sized businesses in formulating business plans, forecasting sales and profits and preparing operational budgets. We also perform multiple types of financial and business analysis services to help managements gain insights and solutions into pressing business challenges. Our business plan formulations and projection services help owners and senior managers plan cash-flows, future expenditures, revenue expansion among others.OHI’s team of financial analysts are skilled in financial analysis tools and have rich experience across sectors such as real estate (commercial and residential), retail, ecommerce, logistics, IT services and small scale manufacturing.

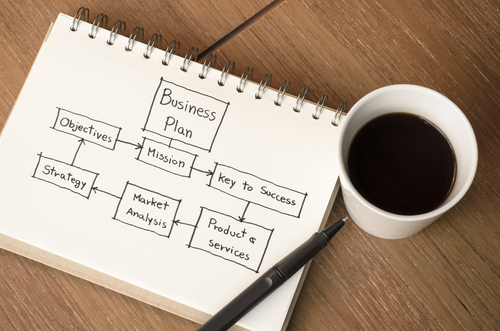

Preparation of detailed business plans with market summary, product/service summary, SWOT analysis, competition analysis, financial projections and more.

Simple financial business plan formulation services covering:

We have prepared 100+ business plans for residential real estate, commercial real estate, retail, restaurants, e-commerce, small manufacturing, wholesale distribution, IT and media services companies.

Budgeting is a critical yearly activity done in most organizations to plan for financial performance, control expenses and allocate capital and resources. Budgeting models have to be dynamic, detailed easy to understand to ensure regular and seamless updating of budgetary numbers and to drive organizational acceptability and accountability. OHI in-depth budget preparation services ensure an accurate, comprehensive and easy to understand budgets. We also use a variety of methodologies such as historical cost basis, % of revenue, bottoms-up budgeting among others.

Financial analysis is crucial in obtaining an understanding of your company’s financial performance. We specialize in providing outsource financial analysis and modeling services. We focus on helping businesses analyze data better and make smart decisions. Our financial analysis outsourcing services provide information regarding the efficiency, profitability, liquidity and stability of the company.

Our indicative standard charges for business plan preparation and financial analysis services are listed below. Custom packages of 25, 50 and 80 hours per month are available.

Financial Analyst is a specialist profile used for financial modeling, business plan formulation, business research and financial analysis assignments. They are responsible for preparation of project reports, financial modeling, management reporting, analysis of financial statements, simple valuations and other custom tasks.