How to Manage Rental Property Accounting: The Ultimate Guide

- June 19, 2026

- OHI

Contrary to popular belief, there is so much more to managing rental properties than just collecting rent and maintaining them. Financial management plays a major role in determining whether a rental business remains profitable or turns into a constant source of stress.

It is exactly where rental property accounting can become useful. It can help landlords as well as property managers to track income, expenses, taxes, and financial records. Without proper accounting, it becomes difficult to understand profits, manage cash flow, or prepare taxes correctly.

As per the U.S. Census Bureau, nearly 36% of households in America live in rental homes. This shows how large the rental market has become and why proper accounting for rental properties is important for landlords and property managers.

In this guide, you will learn everything about rental property accounting, including important procedures, financial reports, software, and mistakes to avoid.

Rental property accounting is essentially the process of recording and managing all financial activities related to rental properties. It includes:

According to Grand View Research, the global property management software market is expected to cross $5.89 billion by 2033 because of increasing demand for automation.

Still, there are many new landlords who start by using a simple notebook or a basic spreadsheet. While this might work for a few months, it quickly becomes a nightmare as your business grows. Professional rental accounting is about more than just knowing how much is in your bank account; it is about building a scalable business.

The primary reason to master accounting in property management is to pay only what you owe in taxes. The government allows you to deduct a wide range of expenses, from property taxes and insurance to the mileage you drive to inspect a unit.

If you don’t have a record of a $50 repair, you can’t deduct it. Over a year, these missed “small” expenses can even add up to hundreds and thousands of dollars in lost tax savings.

Not every property is a winner. By using detailed rental property management accounting, you can see exactly which units are costing too much in maintenance or which ones have the highest vacancy rates.

This data allows you to make smart decisions about whether to sell a property or increase the rent.

If you are ever audited, the IRS or local tax authorities will want to see proof of every transaction. A professional system ensures you have a “paper trail” for every dollar. Furthermore, keeping clear records protects you in legal disputes with tenants regarding security deposits or unpaid rent.

Managing rental property finances becomes much easier when you have a proper financial system in place. Many landlords struggle with accounting because they start tracking income and expenses without any structure. Over time, this creates confusion, missed payments, tax problems, and inaccurate reports.

Here are the most important steps to build an effective rental property accounting system.

One of the first things landlords should do is separate personal and rental finances. Using the same account for both can create accounting confusion and tax complications. A separate business account helps you clearly track rental transactions.

You should ideally have:

Rental property owners usually choose between two accounting methods.

1. Cash Basis Accounting

This method records transactions only when money is received or paid. It is best when used by small landlords, beginners, and owners who only have a few rental units.

2. Accrual Basis Accounting

This method helps to record income and expenses when they occur, even if payment happens later. It is best suited for large rental portfolios, property management companies, and businesses with multiple vendors and tenants.

Choosing the correct method in the early stage helps maintain consistency in financial reporting.

Expense tracking is a lot easier when everything is organized properly. Create categories such as:

This helps you understand where your money is going and simplifies tax deductions.

Manual spreadsheets may work in the initial stage, but they can become difficult to manage as properties grow. Good rental accounting or property management software helps automate tasks like rent collection, expense tracking, invoice management, financial reporting, and payment reminders.

Popular tools like QuickBooks, Buildium, and AppFolio are commonly used in rental property management accounting.

Keeping physical receipts and paperwork often leads to missing documents. Instead, store important files digitally, including lease agreements, repair invoices, tax records, utility bills, and vendor contracts.

Digital records are way easier to access, organize, and share when needed.

Do not wait until tax season to check your finances. Review reports every month to monitor:

Regular reviews are necessary as they can help landlords identify problems early and make better financial decisions.

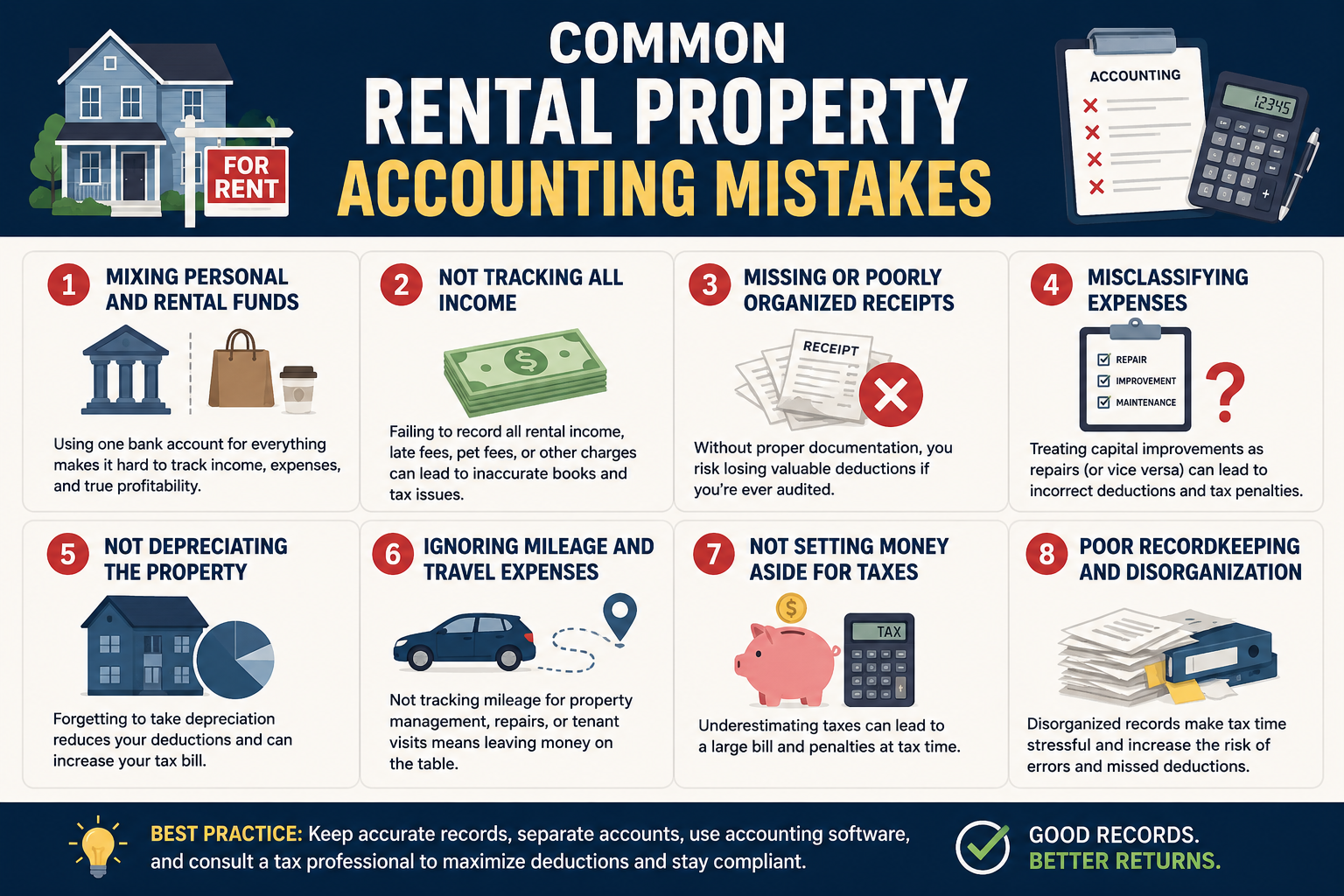

Many landlords tend to make minor accounting mistakes that will eventually turn into bigger financial problems. Poor rental property accounting can affect cash flow, taxes, profitability, and even legal compliance. The good part is that a lot of these mistakes can be avoided with proper systems and regular tracking.

Here are the most common mistakes property owners make more than they realize:

Using only one bank account for everything creates confusion and makes expense tracking difficult during tax season.

Missing invoices, receipts, or lease documents will eventually create a lot of concerns when it comes to audits or tax filing.

Not matching records with bank statements can result in unnoticed errors or duplicate entries.

Waiting months to update important records can eventually lead to missed expenses, forgotten payments, and incorrect reports.

Many landlords focus only on rental income and forget to monitor maintenance, vacancies, and unexpected costs.

Spreadsheets are definitely complex to manage as rental portfolios grow, increasing the risk of accounting mistakes.

When it comes to rental property, accounting can prove to be the difference between owning a hobby and running a business. When you separate your finances, choose the right accounting method, and leverage modern technology, you can protect your assets as well as maximize your wealth.

As your rental portfolios grow, manual accounting tends to become difficult and time-consuming. Thus, by using accounting software and outsourcing accounting for rental properties, it can significantly improve efficiency, reduce errors, and also save valuable time.

Whether you manage one property or a large portfolio, strong property management accounting procedures can help improve long-term business performance.

Rental property accounting includes tracking different aspects such as rental income, expenses, maintenance costs, taxes, as well as financial records, which helps to manage rental properties in an effective way while maintaining long-term profitability.

Some of the popular rental accounting software options include QuickBooks, Buildium, AppFolio, Baselane, and Xero, depending on portfolio size, reporting needs, and automation requirements.

Cash basis accounting is when income and expenses are recorded only when money is received or paid. It is therefore great for smaller rental property businesses.

Separate accounts improve financial organization, simplify tax filing, reduce accounting confusion, and make rental property management accounting much easier to handle professionally.

Yes, it can be very beneficial, as organized rental accounting helps simplify tax filing, supports accurate deductions, reduces compliance risks, and helps landlords maintain complete documentation throughout the year.